Rachel Springall, Finance Expert at Moneyfacts, said:

“Lenders had mixed attitudes to pricing during July, and the churn of products resulted in a dip in choice, cancelling out the previous month’s rise. In spite of the perhaps cautious approach, rate cuts prevailed to push the Moneyfacts Average Mortgage Rate down to 5.04% at the start of this month, edging ever so closer to dipping below 5%. Breaking down into fixed rate moves over the past six months shows where the bigger margins are being shaved off by lenders, with the average two-year rate dropping by 0.51% versus just 0.31% cut off the five-year rate. However, the movement to swap rates has shown a shift back to a more traditional market, where five-year deals were known to cost extra. Such rate inversion has occurred for almost three years, starting in response to the ‘mini-Budget’ in September 2022.

“As it stands, lenders may well consider a more low and slow approach to making cuts over the next few weeks, because of the knife-edge base rate decision last week which led to a rise in swap rates. Piling onto this, the markets could react badly to any significant decisions made in the Autumn Budget, an event which can be a blessing or a curse for future rate setting. If inflation gets out of control or economic uncertainties spike, borrowers can forget about more base rate cuts by the Bank of England this year.

“It has now been two years since the average two-year fixed mortgage rate hit a 15-year high, as lenders frantically repriced their deals the average shelf-life of a mortgage was just 13 days. Lenders are still churning their ranges today, albeit with a shelf-life of 17 days, but such repricing is to the benefit of borrowers. The incentive to refinance today onto a fixed deal is much more critical, as there is now a significant difference of more than 2% to escape a revert rate, compared to just 1% back in August 2023, based on the average two-year fixed rate versus the average Standard Variable Rate (SVR).

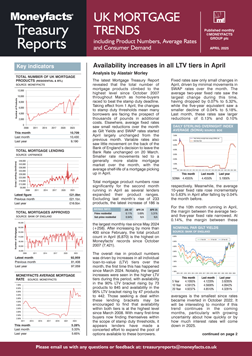

“Borrowers who have a 10% deposit or equity may be pleased to see an uptick in product choice month-on-month, but it is at this tier that the average rate across two- and five-year fixed loan-to-values (LTVs) rose, albeit by small margins. First-time buyers who have a small deposit of 5% will find product choice hasn’t surged as they might have hoped after the Government replaced the Mortgage Guarantee Scheme in July, but in good news there has been a drop to fixed rates. However, the big difference to first-time buyers and those borrowing at higher LTVs as the year progresses will be the changes to the loan-to-income (LTI) rules. Lenders would be wise to do as much as they can to support new buyers, and it remains essential borrowers seek advice to navigate the mortgage maze.”

Rachel Springall, Finance Expert at Moneyfacts, said:

“Lenders had mixed attitudes to pricing during July, and the churn of products resulted in a dip in choice, cancelling out the previous month’s rise. In spite of the perhaps cautious approach, rate cuts prevailed to push the Moneyfacts Average Mortgage Rate down to 5.04% at the start of this month, edging ever so closer to dipping below 5%. Breaking down into fixed rate moves over the past six months shows where the bigger margins are being shaved off by lenders, with the average two-year rate dropping by 0.51% versus just 0.31% cut off the five-year rate. However, the movement to swap rates has shown a shift back to a more traditional market, where five-year deals were known to cost extra. Such rate inversion has occurred for almost three years, starting in response to the ‘mini-Budget’ in September 2022.

“As it stands, lenders may well consider a more low and slow approach to making cuts over the next few weeks, because of the knife-edge base rate decision last week which led to a rise in swap rates. Piling onto this, the markets could react badly to any significant decisions made in the Autumn Budget, an event which can be a blessing or a curse for future rate setting. If inflation gets out of control or economic uncertainties spike, borrowers can forget about more base rate cuts by the Bank of England this year.

“It has now been two years since the average two-year fixed mortgage rate hit a 15-year high, as lenders frantically repriced their deals the average shelf-life of a mortgage was just 13 days. Lenders are still churning their ranges today, albeit with a shelf-life of 17 days, but such repricing is to the benefit of borrowers. The incentive to refinance today onto a fixed deal is much more critical, as there is now a significant difference of more than 2% to escape a revert rate, compared to just 1% back in August 2023, based on the average two-year fixed rate versus the average Standard Variable Rate (SVR).

“Borrowers who have a 10% deposit or equity may be pleased to see an uptick in product choice month-on-month, but it is at this tier that the average rate across two- and five-year fixed loan-to-values (LTVs) rose, albeit by small margins. First-time buyers who have a small deposit of 5% will find product choice hasn’t surged as they might have hoped after the Government replaced the Mortgage Guarantee Scheme in July, but in good news there has been a drop to fixed rates. However, the big difference to first-time buyers and those borrowing at higher LTVs as the year progresses will be the changes to the loan-to-income (LTI) rules. Lenders would be wise to do as much as they can to support new buyers, and it remains essential borrowers seek advice to navigate the mortgage maze.”