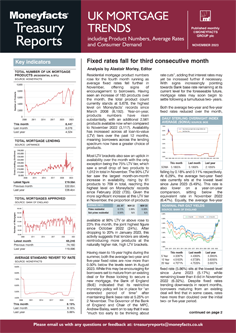

Rachel Springall, Finance Expert at Moneyfacts, said:

“Borrowers searching for a new mortgage deal may be delighted to know fixed mortgage rates continued their downward trend, with the average two-year fixed rate dropping by its biggest margin (0.37%) since December 2022. Those borrowers who have waited patiently in recent months to re-finance, or indeed are preparing for when their mortgage deal expires, would be wise to review rates, as lenders are closely monitoring the volatile swap rate market, which tends to influence fixed rate pricing. There have been big expectations for fixed rates to fall further, and whether now is the right time to refinance will come down to an individual’s circumstances. Lenders are in constant review of their ranges, and it is likely rates will fluctuate in the coming weeks due to the noises surrounding future rate expectations.

“The recent observations made by the Bank of England would suggest base rate is unlikely to move for a few months yet, and indeed the Monetary Policy Committee will wait for firm evidence that inflation is under control before even considering a rate cut. Borrowers who are sitting on their Standard Variable Rate (SVR) should be incentivised to switch their mortgage if they can, as it’s unlikely they will see their repayments drop for the foreseeable. Indeed, the average two- and five-year fixed rates are much lower than the average SVR. Seeking advice from an independent broker is wise to work out if an individual could save a decent sum on their monthly repayments by changing their mortgage deal.

“Those borrowers who are looking to get on the property ladder as a first-time buyer may be pleased to know rates have come down month-on-month. Indeed, the average two-year fixed rate mortgage at 95% loan-to-value has dropped below 6% for the first time since May 2023 (5.94%), much lower than six months ago, when it was just over 7%. Product choice has also increased at this LTV bracket and, while it’s a slight improvement month-on-month, it is encouraging and demonstrates lenders are still keen to support borrowers with small deposits. However, we have seen some product availability drop around other higher LTV brackets, at 90% and 85% month-on-month, so it will be interesting to see whether there will be further declines in these areas over the next few months, or if it’s a short-term adjustment. Lenders are actively reviewing their ranges, so product choice could remain volatile, but borrowers must be quick to check deals as the average shelf-life stands at 28 days, the highest in a year.”

Rachel Springall, Finance Expert at Moneyfacts, said:

“Borrowers searching for a new mortgage deal may be delighted to know fixed mortgage rates continued their downward trend, with the average two-year fixed rate dropping by its biggest margin (0.37%) since December 2022. Those borrowers who have waited patiently in recent months to re-finance, or indeed are preparing for when their mortgage deal expires, would be wise to review rates, as lenders are closely monitoring the volatile swap rate market, which tends to influence fixed rate pricing. There have been big expectations for fixed rates to fall further, and whether now is the right time to refinance will come down to an individual’s circumstances. Lenders are in constant review of their ranges, and it is likely rates will fluctuate in the coming weeks due to the noises surrounding future rate expectations.

“The recent observations made by the Bank of England would suggest base rate is unlikely to move for a few months yet, and indeed the Monetary Policy Committee will wait for firm evidence that inflation is under control before even considering a rate cut. Borrowers who are sitting on their Standard Variable Rate (SVR) should be incentivised to switch their mortgage if they can, as it’s unlikely they will see their repayments drop for the foreseeable. Indeed, the average two- and five-year fixed rates are much lower than the average SVR. Seeking advice from an independent broker is wise to work out if an individual could save a decent sum on their monthly repayments by changing their mortgage deal.

“Those borrowers who are looking to get on the property ladder as a first-time buyer may be pleased to know rates have come down month-on-month. Indeed, the average two-year fixed rate mortgage at 95% loan-to-value has dropped below 6% for the first time since May 2023 (5.94%), much lower than six months ago, when it was just over 7%. Product choice has also increased at this LTV bracket and, while it’s a slight improvement month-on-month, it is encouraging and demonstrates lenders are still keen to support borrowers with small deposits. However, we have seen some product availability drop around other higher LTV brackets, at 90% and 85% month-on-month, so it will be interesting to see whether there will be further declines in these areas over the next few months, or if it’s a short-term adjustment. Lenders are actively reviewing their ranges, so product choice could remain volatile, but borrowers must be quick to check deals as the average shelf-life stands at 28 days, the highest in a year.”